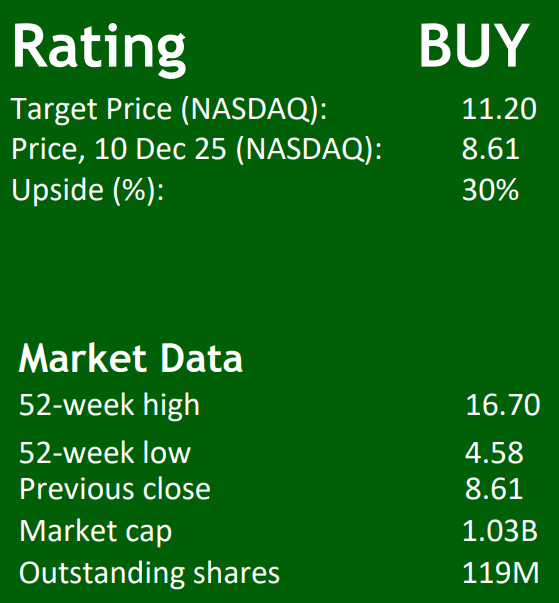

Emerging US Defense Drone Manufacturer

NASDAQ Ticker: RCAT

Red Cat is an emerging US defense drone manufacturer positioned directly in front of two major shifts in global security. Warfare is moving rapidly toward unmanned systems, and rising geopolitical tension is driving structurally higher defense spending across the US and NATO. Red Cat’s platforms across Teal, FlightWave and Blue Ops place it in the slipstream of that demand.

Significant manufacturing capability increased in 2025

Red Cat’s original footprint sits in a 26,000 ft facility in Salt Lake City, UT— space the company doubled in 2025 after winning the U.S. Army Short-Range Reconnaissance Program of Record. The line can now turn out more than 1,000 Black Widow air-frames per month, up from 100 units a month in mid-2023. Giving RCAT the scalable, fully domestic pipeline needed to satisfy both the 5,880-drone Army order and fast-growing NATO demand. Meanwhile, the firm’s brand-new 155,000 ft² “Blue Ops” campus in Valdosta, Georgia—opened in August 2025—houses a rail-served steel and composite hall that will build up to 500 unmanned surface vessels per year, extending RCAT’s manufacturing reach from airborne to maritime domains and supporting management’s guided path to $80-120 million in 2025 unmanned Aerial Vehicle (UAV) which on June 6 2025, President Trump signed an executive order to speed the drone production and enhance the industry.

Business Description

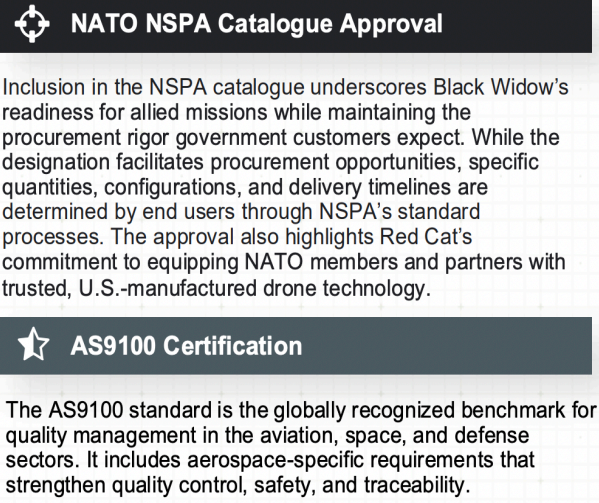

Red Cat Holdings, Inc. (NASDAQ: RCAT) is a vertically-integrated defense technology company that designs, manufactures and supports AI-powered unmanned systems across air, land and sea. Headquartered in Puerto Rico with primary production in Salt Lake City, UT and Valdosta, GA, the Company operates three revenue segments: (1) MIL-SPEC small unmanned aircraft systems (sUAS) sold to U.S. and allied militaries under the Black Widow™ and Teal 2™ families; (2) modular vertical-take-off drones, gimbals and RF sensors for special-operations and law-enforcement customers; and (3) Blue Ops™ unmanned surface vessels (USVs) sized from 12 ft to 40 ft for mine counter-measure, logistics and coastal-patrol missions. All platforms are National Defense Authorization Act (NDAA) compliant, with partnerships such as Palantir, IED detection and autonomous navigation without cloud connectivity. The Company’s 330,000 ft² of production space—expanded 3.7× in the last twelve months—can currently output 4,000 Black Widow air-frames, 15,000 FPV tactical drones and 500 USV hulls per year, giving RCAT the scalable, U.S.-sourced capacity demanded by its five-year, 5,880-unit Short-Range Reconnaissance Program-of-Record with the U.S. Army and a growing NATO Foreign Military Sales pipeline.

Teal Drones

Teal develops UAS for the military and law enforcement. It manufactures products in Utah and is focused on making end users successful in each of their modern operating environments. Teal’s unmanned systems are open, modular, and interoperable.

FlightWave

FlightWave is a California-based aerospace company that specializes in developing long-range, autonomous VTOL drones and sensors. Their flagship product, the Edge 130, is highly versatile and well-suited for both commercial and defense applications.

Blue Ops

Red Cat is committed to dominating the U.S. uncrewed surface vessel (USV) market by delivering bleeding-edge sensor and kinetic strike capabilities that redefine maritime autonomy and lethality. Designed for seamless integration enabling true multi-domain operations across sea, air, and land.

Macro Trends: Tariff Protected, DOD Shift

The Trump administration’s 2025 National Security Strategy (NSS) explicitly recenters U.S. military and industrial policy on “economic security is national security.” That single line is a green-light for companies like RCAT that (a) manufacture inside the United States, (b) use AI and advanced robotics, and (c) ship only NDAA-compliant, traceable hardware to the Pentagon. The NSS calls for “a strong defense-industrial and manufacturing base” and dominance in AI, quantum and super-computing to keep the force technologically ahead of China. RCAT checks every box: Salt-Lake and Georgia plants are AS9100, every flight controller is U.S.-sourced, and its on-board SPOTD AI engine was developed with domestic R&D dollars. In addition, the strategy’s new “Trump Corollary” to the Monroe Doctrine prioritizes hemispheric security, meaning more UAV and USV missions for drug-interdiction, port security and Caribbean littoral patrols—exactly the roles Black Widow and Blue Ops vessels are already funded to perform. Finally, DoD’s Manufacturing Technology (ManTech) program is pouring money into “responsive, world-class manufacturing capability” and next-gen workforce pipelines; RCAT’s 550-person (and growing) U.S. payroll plus its ESAero partner pod put it in the direct funding lane for these capital grants.

Financial Deep Dive: Significant Revenue Projected

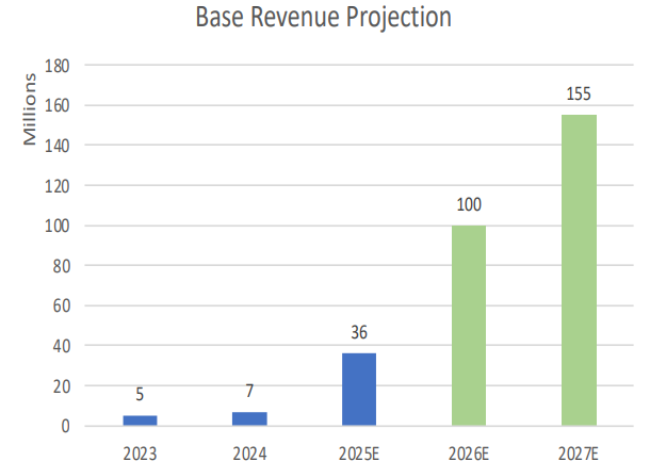

Red Cat’s revenue history shows a textbook pre-contract valley—$7M (’21), $6M (’22), $5M (’23) and $7M (’24)—before the 2025 Short-Range Reconnaissance award flipped the switch: Q1-25 $2.2M, Q2-25 $3.2M, Q3-25 $9.6M and guided Q4-25 $20-23M deliver a full-year midpoint of ~$36M (+440% YoY). Management now guides $80-120M for FY-26 and street models $110-165M for FY-27, a three year CAGR north of 130% that turns a half-decade of sub-$10M sales into a $150M-plus run-rate while gross margin exits negative territory and is expected to reach the mid-teens by late 2026 as volume absorbs the $18.5M of newly deployed Salt-Lake and Georgia capacity.

Healthy Balance Sheet to Cover Future Costs

Red Cat’s balance-sheet history mirrors its revenue arc: thin cash and rising equity dilution from 2021-23 (YE-23 cash $4M, total debt $12M, negative book value) flipped in 2024-25 after three equity and debt issuances for ~$190M of gross proceeds; Q3-25 closed with $212M in cash & equivalents, $22M in low rate notes, and a $150M untapped revolving credit, giving the company an estimated 24-30 months of runway at the current $65-70M annual burn rate even if the $80-120M FY-26 revenue plan slips. Provides them the opportunity to sign long lead contracts without risks of equity dilution.

Cash Flow Story of Investing rather than Bleeding

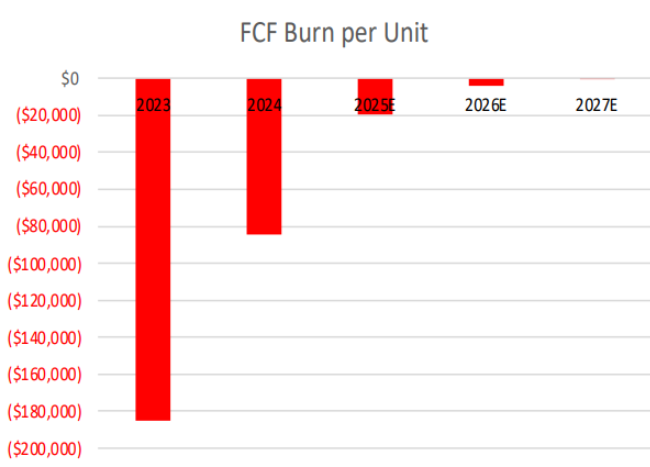

Red Cat’s cash-flow story is still one of building rather than bleeding: over the past twelve months the company poured roughly $68 million into day-to-day operations and another $19 million into new equipment, yet almost two-thirds of that operating outflow was simply the cash needed to stack Black Widow parts in Utah and steel plates in Georgia ahead of the Army’s accelerated delivery schedule. Because every dollar of that build sits against already-awarded, noncancellable contracts, the inventory build is effectively a short-term loan to the Pentagon that will convert to cash as soon as the drones ship and invoices clear. Equity raises in late 2024 and 2025 have covered the entire tab—cash on hand actually rose year-over-year—so while free cash flow is deeply negative on paper, the burn is tied to growth, not a fundamental inability to run the core business at break-even. The only wrinkle to watch is that unbilled receivables are climbing faster than revenue; if Washington’s payment offices slow even slightly, the long-promised 2026 swing to positive operating cash could slip by a quarter, but for now the trajectory is “spend today, collect tomorrow,” not cash flying out the door.

Risks

Execution Risks Remains Present

It is a difficult industry to make money on as you’re dependent on government contracts based on approvals and many sunk costs made into manufacturing facilities. Key risks can come from if they continue to push gross margins. As quantities increase margins will alleviate but until then, their limited capacity has large sunk costs. Additionally, once orders do come online, they need to be able to quickly manufacture and deliver the promised quantities. Some of their Supply chains are concentrated with their IR capabilities that give Black Widow its Night vision edge come from a single vendor which could create a bottle-neck if they were unable to fulfill their promise.

Shareholder Dilution

Red Cat’s growth has been financed largely from the equity tap: since 2021 the company has grown shares outstanding from 54 million to 118 million through a series of PIPEs and an active at-the-market program, meaning early investors now own roughly half the slice they started with. Because the business is still pre-cash-flow and will likely burn $25-40 million in 2026 even under bullish revenue scenarios, management retains a $150 million unused shelf that can be dribbled out at any time. While these sales keep the balance sheet bulletproof and fund plant expansion without debt covenants, they also convert future upside into incremental dilution: every 10 million new shares printed at today’s price erodes EPS by about 8-9 percent and caps how fast per-share metrics can improve once margins turn positive. In short, shareholders are paying for RCAT’s growth twice—once with their patience for losses and again with a steadily shrinking ownership percentage—so any equity raise before operating cash turns positive represents a live, recurring risk that could pressure the stock even if contract wins and revenue beat expectations.

Evaluation

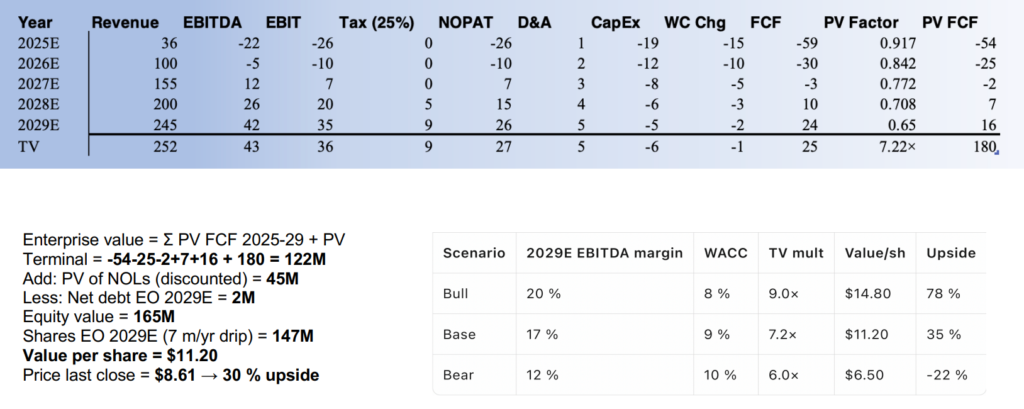

Base Case is Deliberately Conservative

Under the base-case model we only give RCAT credit for the already-awarded Army SRR Tranche-2 (+ small follow-on) and a bare-bones 200-hull USV ramp. That yields $100 M in 2026 revenue—the bottom end of the Street range and $10-15 M below management’s own guide. We further haircut margin progression, exit at 17 % EBITDA (vs. peer primes at 20-25 %) and capitalize no new export wins. In short, we assume:

- No NATO FMS tail (historically $18 M booked Oct-25, with option for 4 more countries)

- No additional Army tranche (Tranche-3 RFP is sole-source, $90-110 M, decision Q2-26)

- No Navy 30-hull option ($25 M contingent on 2026 demo success)

- No Lat-Am or Indo-Pacific export (DJI ban opens 40+ cleared markets)

If those pieces fall in, the top-line moves to $130-160 M in FY-26—exactly the Wall Street consensus band. Flowing that through the same DCF grid (and keeping exit margin at 19 %, still conservative vs. AXON 25 %) lifts 2029 EBITDA to $55 M and the terminal value to $445 M (vs. $180 M in base). Net result: equity NPV jumps to ~$1.9 B, or ~$13 per share, >55 % above today’s price. Thus the current quote only prices the “show-me” scenario; any confirmation of FMS, NATO, or Tranche-3 converts the model from base to bull and pushes the stock into the low-teens without heroic assumptions.

Investment Thesis Wrap Up

Red Cat’s growth is just beginning. We haven’t even discussed how future acquisitions are always on the table for them, which will boost their product portfolio. With an expected ban on Chinese DJI UAS equipment on Dec 23rd, Red Cat will be the only Publicly Traded UAS Company that is fully vertically integrated that is NDAA Compliant. With relationships already integrated with the Army, ramping up further tranches is an advantage they have. To put into context the Budget for the DOD in FY2025, which began in October 1 of 2024, was $74M for Small UAS. Red Cat secured $40M of that budget. For FY2026, which started October 1 of 2025, the SUAS Budget is $747M. The incredible multiple is there for RCAT.