Utility and Infrastructure Play

NASDAQ Ticker: ESOA

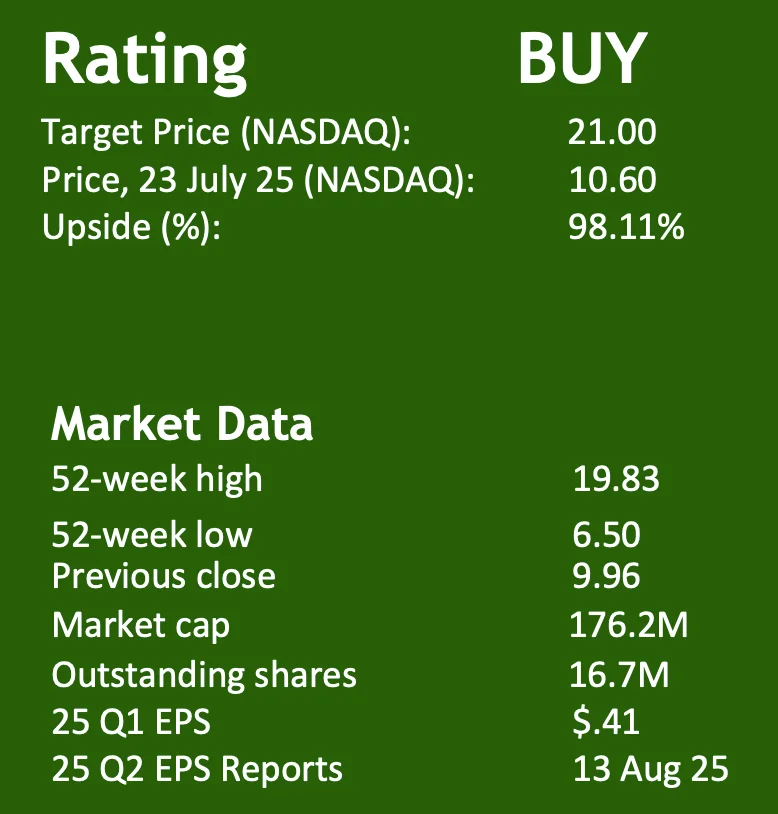

I base the initial BUY rating for Energy Services of America on its growing backlog, low valuations, and under-the-radar infrastructure contractor trading at a deep discount to peers. As of March 31, 2025, the company reported a robust backlog of $280.7 million—representing nearly 1.75x its market capitalization of $160 million. This metric alone reflects substantial visibility into future revenue generation and underscores the disconnect between valuation and operating fundamentals. Recent initiatives to broaden geographic reach and diversify service offerings—achieved through both acquisition and internal expansion—have begun to bear fruit. The successful integration of acquired entities has allowed ESOA to function as a vertically integrated contractor

Despite strong top-line growth—driven particularly by a 30% YoY increase in Gas and Water Distribution revenue during FY24—the company trades at some of the lowest valuation multiples in its sector. A PEG ratio of 0.11 is dramatically below the industry median of 0.87, signaling that the market has not priced in its earnings growth. Additionally, the current EV/Sales ratio of 0.57 compares favorably against a sector median of 2.04, suggesting a significant re-rating potential if growth persists.

Tailwinds: Structural Trends in Infrastructure and Water Access

The rising urgency around water access-both residential needs and industrial purposes like AI datacenter cooling and chip manufacturing- is placing infrastructure providers in high demand. The company’s growing participation in water intensive projects align well with future regulatory and environmental priorities, offering revenue and margin expansion.

Business Description

Headquartered in Huntington WV, they operate six subsidiaries. Cj Hughes construction: They primarily engaged in construction, replacement and repair of natural gas pipelines, water, petroleum, and storage facilities for utility companies and private natural gas companies. Nitro Construction: They provide primarily electrical mechanical, HVAC contractor that provides its services to power, chemical, and automotive industries with commercial capabilities. Provides a full range of electrical and mechanical services such as switchyard services, site preparation, equipment setting, pipe fabrication and installation. West Virginia Pipeline: They assist with maintenance and services of pipelines along WV and surrounding states. SQP Construction Group: General contractor with focus on commercial and industrial buildings and civil work for private/ public companies and state/local governments. TRI State Paving and Sealcoating: Paving utility installation team that is in Hurricane, WV and primarily servicing utility companies in Charleston West Virginia, Lexington, Kentucky, and Chattanooga Tennessee. Ryan Construction Service: Located in WV and primarily serving natural gas distribution and broadband telecommunication customers in Northwestern WV and Pennsylvania. They offer pipeline construction, horizontal directional drilling and corrosion prevention services.

Operational Outlook: Margin Recovery and Strategic Integration

While early 2025 was marked by weather-related delays and integration costs tied to the late 2024 acquisition of Tribute Contracting & Consultants, these headwinds are largely transitory. As high-margin projects resume under more favorable weather conditions and integration costs taper, margins are expected to rebound. The company’s fixed cost structure means that even modest increases in project volume can have outsized impacts on bottom-line results.

Favorable Insider Ownership

With insider ownership of approximately 26%, management’s alignment with shareholder interests appears strong. This level of internal stake holding also signals confidence in long-term value creation, particularly as the company continues to scale through both organic and inorganic means.

Growth at a Bargain Price

ESOA’s strong backlog, improving margins, and multiple growth catalysts—including federal infrastructure spending, index inclusion, and expanding vertical capabilities—are not yet reflected in its current valuation. While near-term volatility may persist due to weather and integration cycles, the underlying trajectory is positive. The confluence of discounted valuation, operational momentum, and strategic expansion supports a BUY rating for investors seeking exposure to essential U.S. infrastructure with asymmetric upside potential.