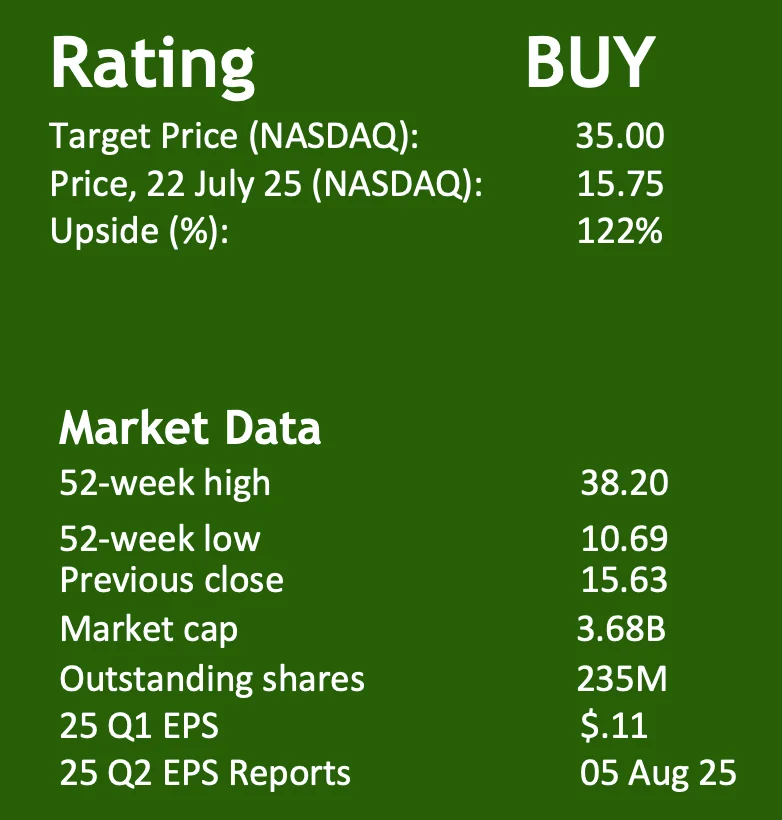

AI Data-Driven Cloud Platform

NASDAQ Ticker: ZETA

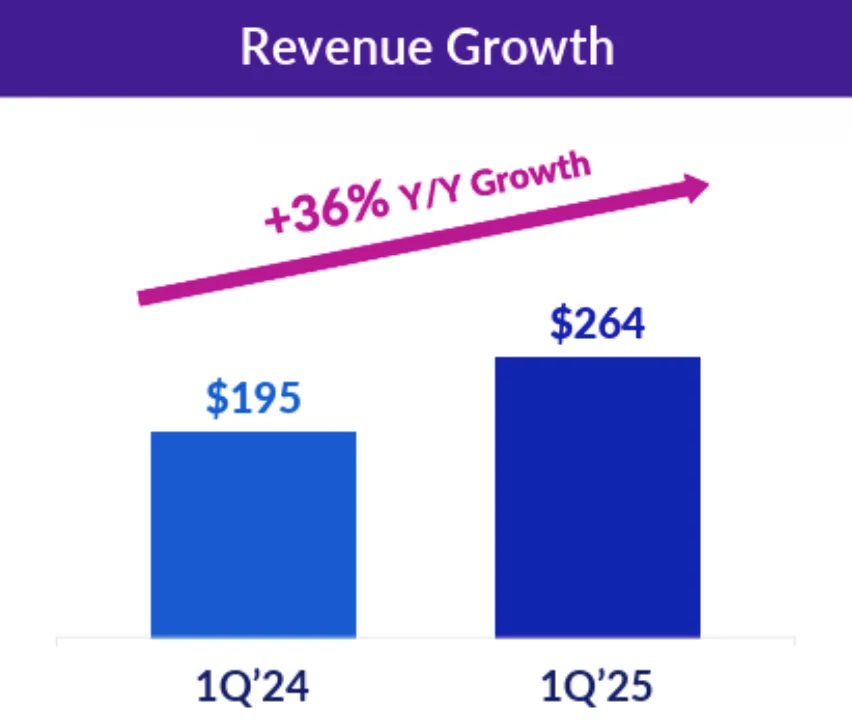

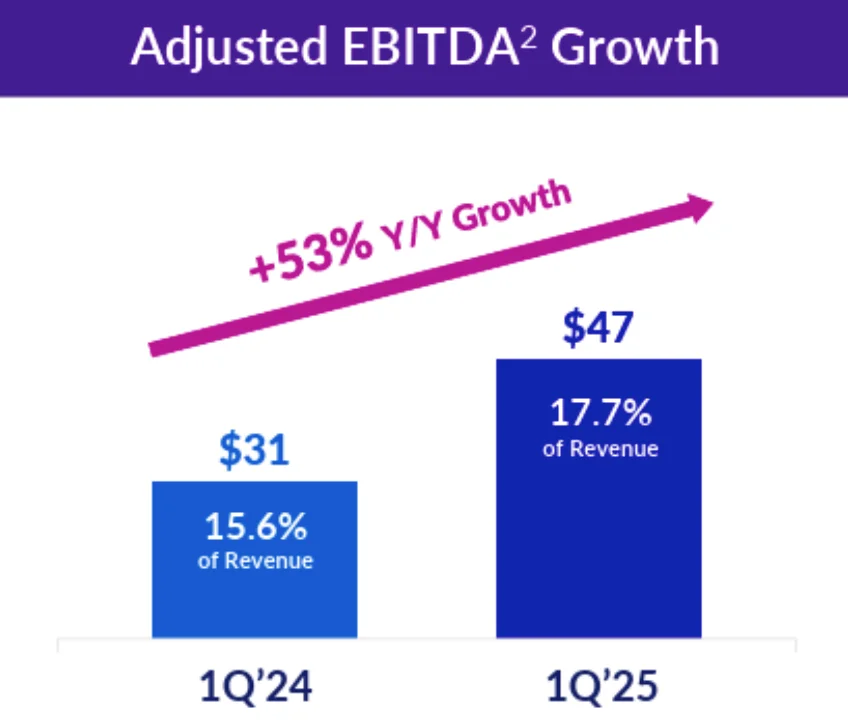

I base the initial BUY rating for Zeta Global on its low valuations for its robust growth metrics and improving profitability. Revenue growth YoY is 40%, significantly higher than the sector’s median of 6%, indicating strong expansion. Additionally, EPS growth FWD is 25% more than the double of the sector’s 11%, highlighting impressive financial performance. In Q1 2025 revenue grew 36% YoY with adjusted EBITDA up 53% reflecting strong cross selling momentum and high Average Revenue Per User. These results point to Zeta’s platform capability to derive high growth even amidst macro uncertainty.

13 Straight Quarters of >20% of Revenue Growth

Looking forward, Zeta’s 2028 plan is targeting over $2B in revenue and Zeta’s current valuation metrics are favorable. For instance, the forward P/S of 2.9x is ~4% below the sector median of 3.1x, and its forward EV/EBITDA of 13.2x is 13% below the sector median of 15x, despite superior growth, 26% forward revenue growth vs. 7.09% sector median and 35.17% forward EBITDA growth vs. 9.22% sector median.

Well Positioned for Expansion

Zeta’s long-term strategy outlines a 2028 target of $2B in revenue, implying a multi-year CAGR well above market norms. The company continues to benefit from secular trends such as AI-powered marketing automation, first-party data solutions, privacy-forward advertising. Zeta’s platform leverages a proprietary data cloud and identity graph as third-party cookies phase out and enterprises prioritize personalization and measurable ROI.

Business Description

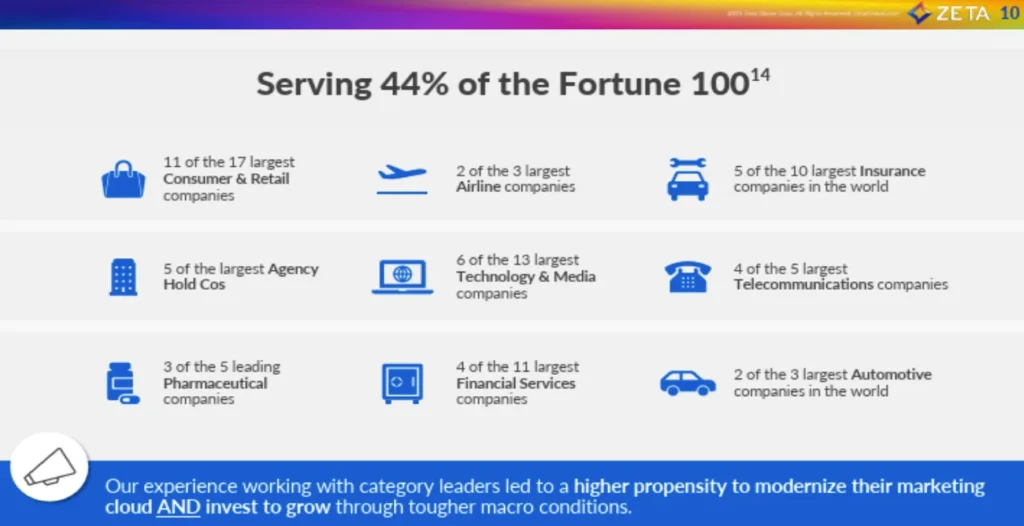

Zeta Global Holdings Corp., headquartered in New York City, operates as an AI-powered omnichannel data-driven cloud platform. Founded in 2007, the company offers enterprises solutions for consumer intelligence and marketing automation through its Zeta Marketing Platform (ZMP). This platform leverages generative AI and machine learning to process billions of data signals, enabling personalized marketing across channels such as email, social media, web, chat, and Connected TV. Zeta’s platform is designed to optimize marketing spend and increase return on investment for its clients by predicting consumer intent and delivering personalized marketing experiences at scale. ZMP’s ability to analyze extensive data sets and leverage AI for precision marketing offers significant advantages in optimizing client marketing spend and enhancing return on investment. Zeta’s partnerships and its focus on innovation position it as a leader in delivering measurable marketing results, differentiating it from competitors who may not offer the same level of integrated AI capabilities.

Customer Retention

Zeta has an ability to retain and scale their customers. They constantly outperform their benchmark for new customer acquisition cost and their ability to be a repeatable, scalable solution has led to an increase in commitments. Multiple customers have culminated in the signing of a two-year agreement that doubles their annual investment with Zeta. For example, an insurance customer they assisted in driving their new customer acquisition cost by 37% lower than their 2024 target. This one example quickly demonstrates how valuable Zeta is to their customers and the longer those customers stay with Zeta the more they spend from results they see.

Why the Low Valuation?

In Nov of 2024 a short report from Culper Research claimed issues with Zeta’s business practices including accounting, data collection and privacy. During this period not one Zeta customer left the company, the company refuted and had a third independent accounting firm verify its GAAP, and calmly bought back over 1.6M shares because of the confidence the team has in its stock.

Zeta’s 2028 FCF Plan and Growth Story is a Force to Be Reckoned With

Zeta’s impressive YoY 40% growth with a continued implied minimum 20% CAGR, implied 25% margin, and implied 65% Free Cash Flow conversion is a force to be reckoned with. It is only a matter of time before the market recognizes how heavily undervalued this stock is at $15 a share. This fits phenomenally into the portfolio because its growing, healthy, profitable, and it touches the topic of AI which will help boost its stock once momentum is along with it.