Designs, Produces, Seller of Avionic Solutions

NASDAQ Ticker: ISSC

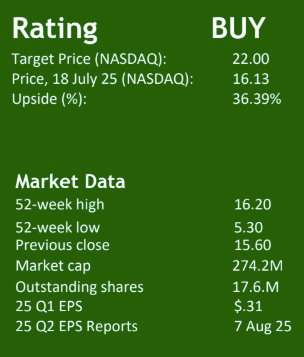

I base the initial BUY rating for Innovative Solutions and Support, Inc. on its current growth prospects and projected free cash flow. Revenue has grown 168%, from $17.6M in 2019 to $47.2M in 2024. On June 30, 2023, ISSC acquired certain assets and granted perpetual license rights to manufacture and sell licensed products related to Honeywell’s inertial, communication, and navigation product lines. This integration has propelled them into a new market of aerospace and military products, where they are well-positioned to capture market share.

Revenues up 168% since 2019 and Are Only Expected to Rise

The compounded annual growth rate (CAGR) of ISSC since 2019 averages roughly 19% per year, while its operating income CAGR has simultaneously reached 37%. Improving both revenue and margins illustrates management’s disciplined focus on profitability while growing the company. The strong operating income improvement has been driven by the ability to pass through raw material cost increases, increased capacity utilization resulting in lower operating costs (i.e., reducing their fixed cost per unit), operating leverage created through sales growth, and a favorable product mix.

Well Positioned for Current Administration Tailwinds.

With headquarters in Exton, Pennsylvania, and a recent expansion of that facility to triple its production capacity, ISSC supports American-made equipment. On June 6, 2025, President Trump signed an executive order to accelerate drone production and enhance the industry, placing ISSC in a favorable position to benefit from this policy shift.

Business Description

ISSC, headquartered in Pennsylvania, is a systems integrator specializing in the design, development, manufacture, sale, and servicing of avionics products and systems. The company operates in the aerospace sector, offering flight guidance systems, auto-throttles, cockpit display systems, and a variety of communication and navigation products. ISSC serves a diverse clientele, including commercial air transport carriers, corporate and general aviation companies, the U.S. Department of Defense, foreign militaries, and original equipment manufacturers (OEMs). The product lineup includes air data products, flat panel displays, flight management systems, inertial reference systems, and more. Its recent acquisition of product lines from Honeywell International has bolstered ISSC’s capabilities in military displays and flight control computers, expanding its opportunities in defense markets.

Macro Trends

Tariff Protected, DOD Shift, AI Products in the Making

They have a next-generation AI-enabled Utility Management System, which will fit perfectly in the growing demand for drone production. With the initial focus being on military customers and applications, they have established relationships with those customers to help win contracts. In preparation of the transition and planned product expansion for military capabilities, ISSC doubled its footprint and tripled its production capabilities. Impressively, the construction project cost the company around $6M, which has been funded purely by operating activities.

Future Acquisitions on the Radar

The company plans to continue to target acquisitions. “Deploying capital for strategic acquisitions remains a high priority.” They anticipate focusing on complementary product lines from other suppliers and continuing to expand their products.

Financial Results

Net revenue in Q2 totaled $21.9M for 2025. Gross profit was $11.3M with a gross margin of 51.4%, up sequentially from 41.4% in Q1. They generated more normalized gross margins under Honeywell contracts, which was the main driver of improved gross margin. Operating expense was $4.3M, representing 19.6% of revenue, down from 36.7% YoY. Backlog as of March 31 was $80M. Cash Flow from operations was $1.3 M FCF was negative 300K due to facility expansion.

Investment Thesis Wrap Up

Strong Organic and Inorganic Growth to Continue

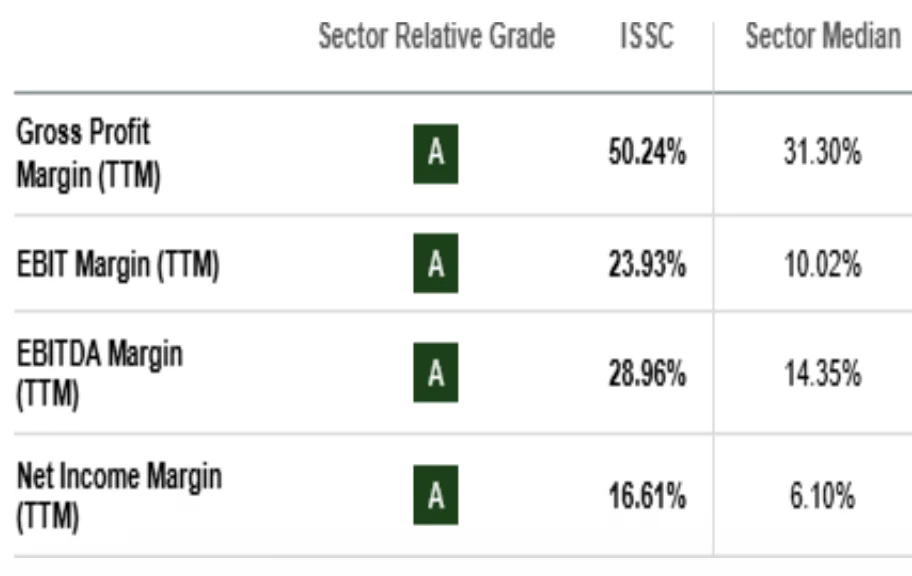

The current management is calling for 30% growth in revenue and net income, while the company has reached $80 Million in backlog sales. This shows that with expected revenues of $61.1M and NI of $9 Million. This fits our perfect template of growing revenue, growing margins. Additionally, to hammer in their efficiencies, their gross margins and NI margin are ~50% and 16% respectively, while the Sector Median is 31% and 6% respectively.