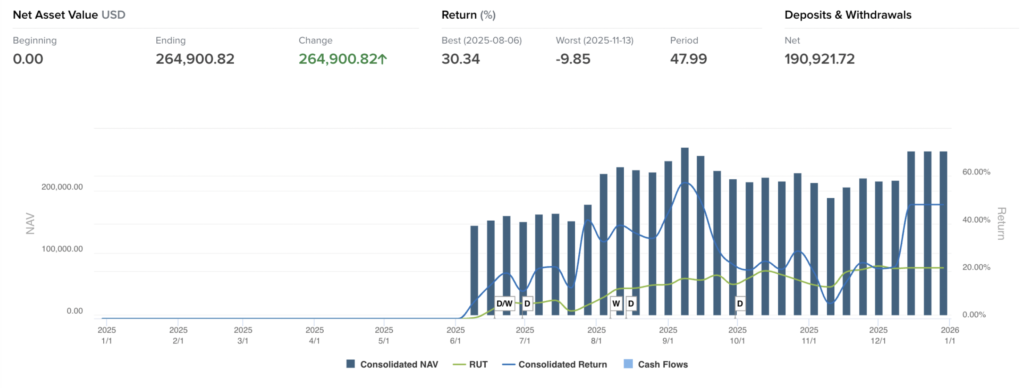

We are pleased to report that Capital Growth Fund LLC generated a return of 47.99 % in calendar-year 2025, outperforming the Russell 2000 by 4,787 basis points and placing the partnership in the top-decile of our small-cap peer group. The result was driven by a concentrated, catalyst-rich book that benefited from both company-specific inflections and an acceleration in U.S. defense procurement that began with the enactment of the FY -2026 appropriations on 1 October.

Performance Attribution:

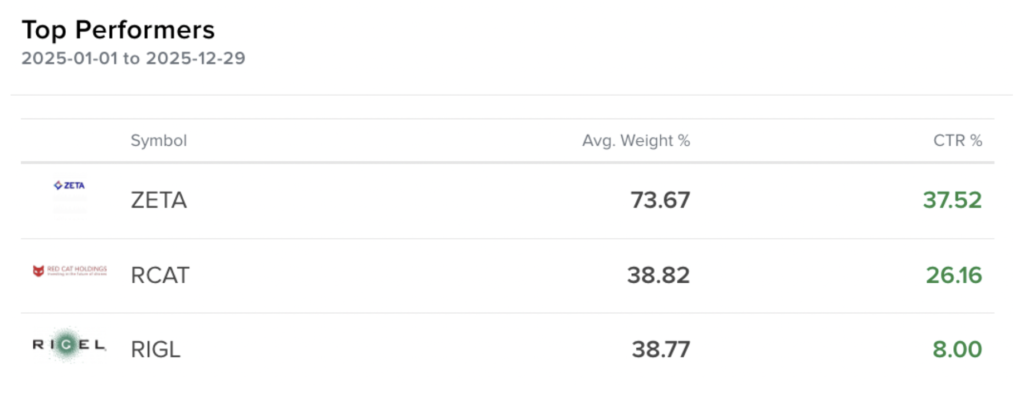

- Core long book: Our top three positions contributed significantly when we found an entry point while they were highly mispriced.

- Event-driven sleeve: Red Cat Holdings (RCAT) appreciated sharply after the U.S. Federal Aviation Administration banned Chinese-manufactured DJI drones on 23 December, instantly elevating RCAT’s U.S.-built vertical as the only compliant, scalable alternative for government and enterprise customers.

- Macro overlay: Episodic volatility, triggered by concerns of an AI-related market bubble—created dislocations that we exploited to build positions at more favorable risk-adjusted entry points.

Executive Summary

- One Share at Inception = $1,000.00

- One Share at End of 2025 = $1,442.31

- Net Fund Return (Annual 2025): +47.99%

- Benchmark (Russell 2000): +11.3%

- AUM: $265K

- ZETA: AI-native marketing-cloud platform that enables consumer brands to bypass traditional ad-tech intermediaries. By unifying first-party data, predictive modeling, and omnichannel execution, ZETA reduces customer-acquisition costs by up to 30 % while converting campaign spend into high-margin, recurring SaaS revenue.

- RCAT: A U.S.-based, fully vertically integrated drone manufacturer that designs, builds and deploys autonomous systems from its own facilities located in Salt Lake City and others. They already carry multi- year, sole-source contracts with the U.S. Army for reconnaissance and loitering-munition platforms.

- RIGL: Core business is turning its oral spleen-tyrosine-kinase (SYK) blocker Tavalisse into the go-to, steroid-sparing therapy for chronic ITP; in Q3 it shipped 8,550 bottles, +19 % seq., driving $25 M in U.S. Tavalisse net sales that beat the Street by $3 M and pushing total revenue to $40 M versus the $34 M consensus. Management also guided 2025 Tavalisse sales to the upper half of the $90-100 M range, showing their growth expectations.

In short, all three names carried “torque”: small share counts, fixed cost bases, and customer catalysts big enough to make the incremental movements big for us.

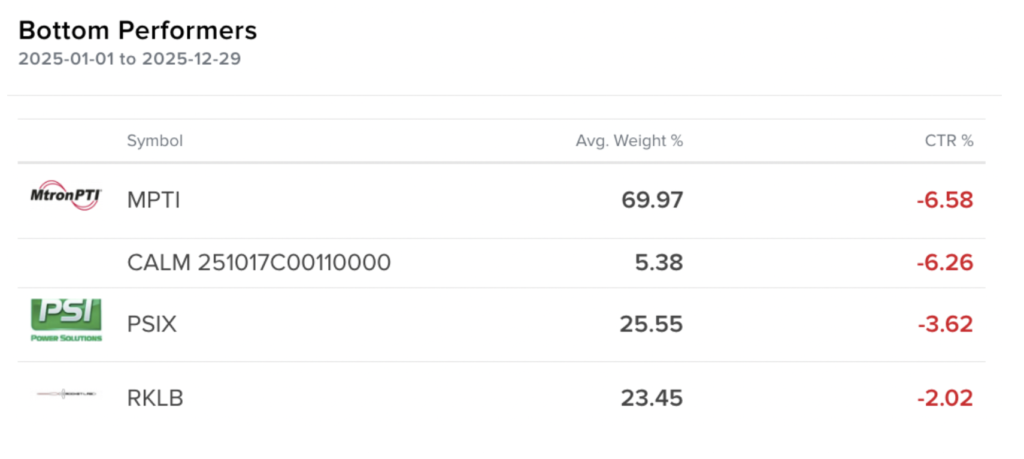

- MPTI: Supplies radio frequency components that help with the accuracy of radio hopping for military and commercial vehicles. Their ability to win contracts and grow is substantial. We entered at a trough but with a small position.

- PSIX: Original-equipment manufacturer of industrial engines used in back-up power systems for data- center build-outs. Revenue trajectory remains intact, yet the stock is discounted on AI-related risk-off sentiment.

- RKLB: Designer and producer of satellites, antennas, and launch vehicles with a growing pipeline of domestic and international contracts. We exited the position on technical criteria, but continue to monitor for an improved entry.

In short, each of these companies are still attractive, fundamentally sound companies, we unfortunately had some technical performance that required us to cut the losses early

Risk Management & Outlook

Our rules-based process continues to emphasize downside protection while preserving optionality to asymmetric upside. Positions must exhibit (i) accelerating revenue, (ii) identifiable forward catalysts, (iii) expanding gross or operating margins, and (iv) net-cash or de minimis balance-sheet risk.

Looking into 2026, we expect small-cap technology, select construction, and certain consumer-staples names to benefit from incremental AI capital expenditure and the lagged effect of Federal Reserve rate cuts. The largest macro risk on our dashboard is a deterioration in U.S. labor-market conditions; rising unemployment could compress discretionary earnings and amplify equity volatility.

Our largest risk we are monitoring:

- Downsides in the Labor Market as unemployment is rising and how the market will react to these fears of a slowing economy.

Closing Remarks

At Thrive Financial Partners, our priority remains delivering consistent, risk-adjusted returns above benchmark while protecting client capital.

We appreciate your trust and look forward to building on this year’s progress.